Despite not being able to invest much, my portfolio has crossed the SGD 1.1 million mark for the first time. Read on for the details.

The first half of 2025 was turbulent, to say the least. The US administration started a trade war, I moved to Switzerland, the markets went up and down – and then straight up again. It was everything but boring.

Portfolio in review:

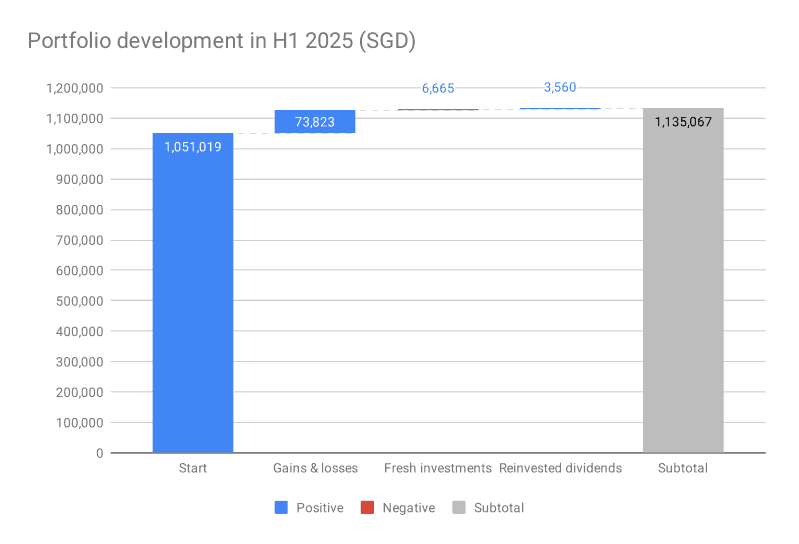

In the first half of 2025, my portfolio increased by SGD 84,048 – from SGD 1,051,019 to SGD 1,135,067. This gain was made up of portfolio returns of SGD 73,823, fresh investments of SGD 6,665, and reinvested dividends of SGD 3,560.

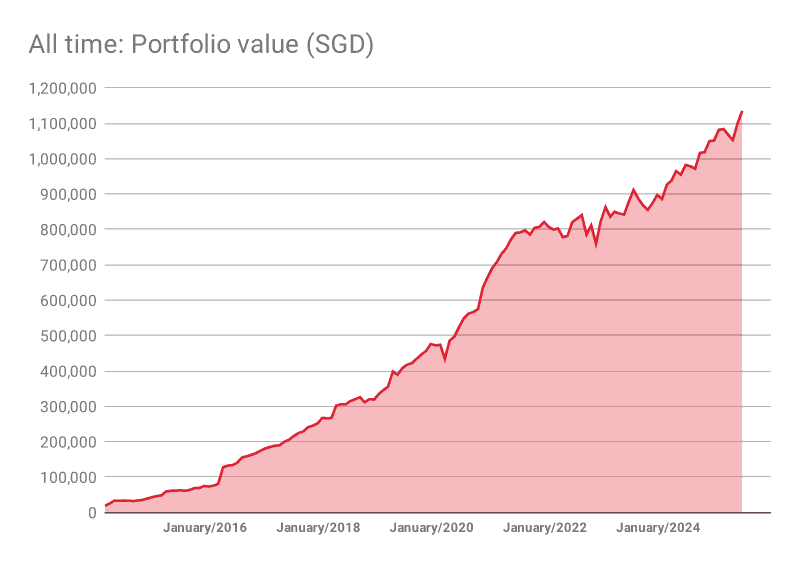

Even though I have not been able to invest much since I quit my corporate job, the portfolio has been growing nicely:

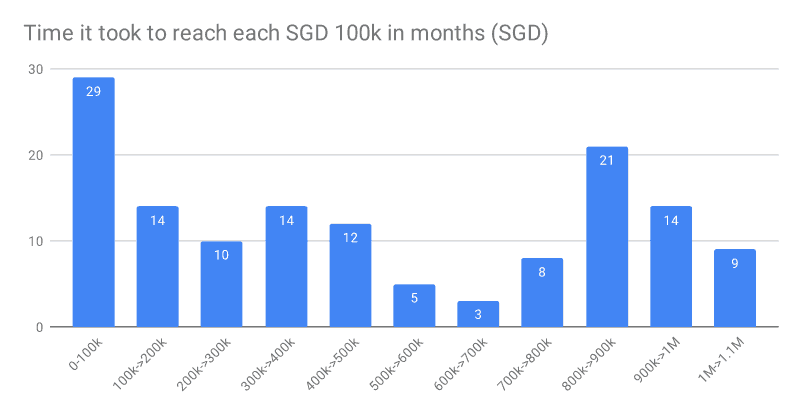

It is true that the first SGD 100,000 is the hardest. Here is a chart showing how many months it took to reach each additional SGD 100,000:

I have not been investing heavily since leaving corporate life in August 2022, so it is remarkable how compound interest continues to do its job.

Portfolio allocation:

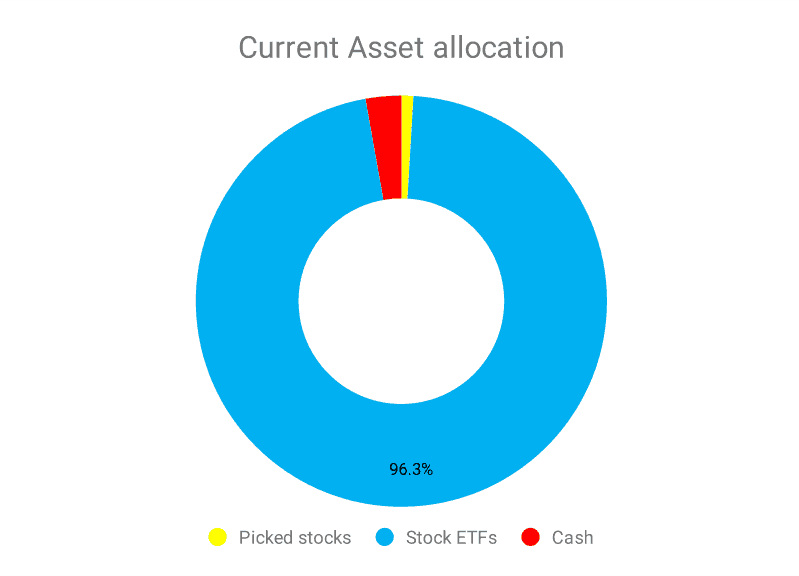

My portfolio is now almost entirely in stock ETFs. During the selloff in April, I sold my remaining bonds and shifted everything into stocks. In hindsight, this worked out well, as stocks have rallied about 15 percent since that time.

I had been planning to exit bonds for a while, mainly because of the tax situation. High taxes on bond dividends made them unattractive in Europe.

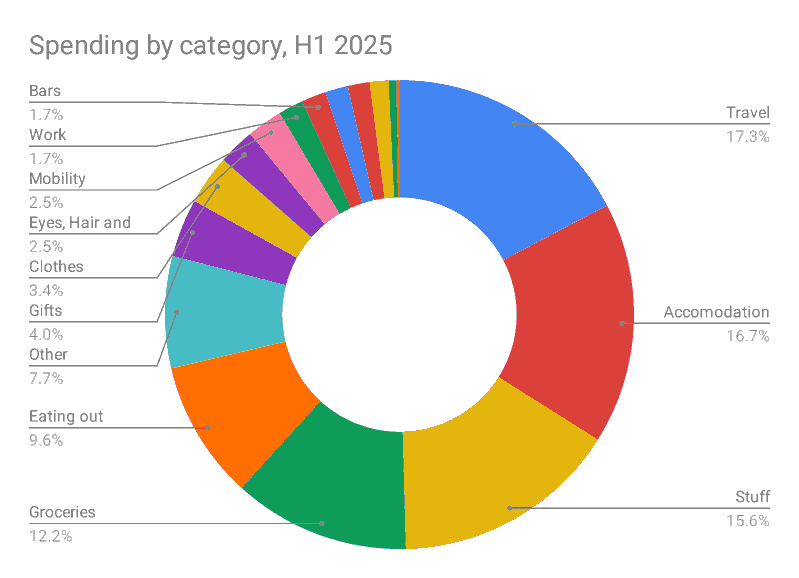

Expenses:

I spent far too much furnishing the new apartment and on travel. Total expenses for the first half of 2025 came to SGD 32,201. This means I only achieved a saving rate of roughly 24 percent. A far cry from the around 70% of my high income years.

My expenses are largely driven by wants rather than needs. I could retire comfortably if I limited spending on wants. It gives me great comfort to know that I have the option to leave the workforce permanently if I choose. I would just need to keep monthly expenses around SGD 3,780. That is difficult in Singapore but quite achievable in many parts of Europe.

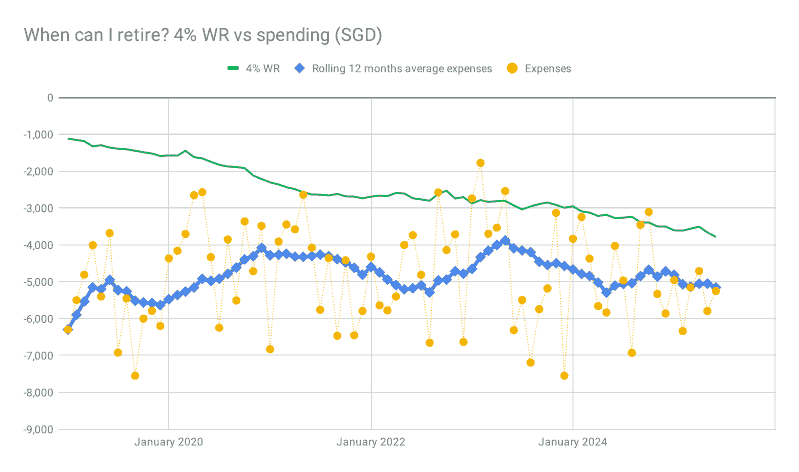

When can I retire, based on current spending?

As soon as the green line and the blue line cross, I could retire at my current level of spending. That is a pretty good position to be in. While I have done a poor job of reducing expenses, I have been consistent with saving, and the green line has been steadily moving in the right direction.

Outlook:

My third year of working for the startup will be complete in September. To be honest, I am growing a bit tired of working. On many days in the home office, I do not get much done, and work has been frustrating me more than it used to. I am really looking forward to retiring for good.