2025 – another mad year is over…

How is life?

I am glad that I managed to leave the office behind at the relatively young age of 40 in 2022.

This morning I woke up at 6:45 after eight hours of excellent sleep. The only reason I felt slightly grumpy was a vivid nightmare about the job I had left years ago. It is striking how deeply work affects the psyche, similar to dreaming about school exams decades later.

My wife’s remote job ended, and she now works full time from an office in Switzerland. She earns very well, but this also means that I have to spend most of the year here. Switzerland is beautiful, so that is acceptable. Unfortunately, my tax residence is still Germany, which is far less acceptable from a tax perspective.

One minute walk from our apartment. Switzerland is rather okay…

My wife and I keep our finances separate out of habit and laziness. Her income, portfolio, and expenses are not part of this blog, which I started long before getting married. That said, she earns a ton of money in Switzerland, and her portfolio has been growing quickly. It is still smaller than mine, but she is catching up fast.

My job is … ok lah. Periods of high intensity, stress, and business travel alternate with calmer phases. Since the startup is small, I do not have many meetings. This gives me flexibility to exercise during the day or work at weird hours. Also sometimes I take glorious naps in the middle of the day.

Portfolio update

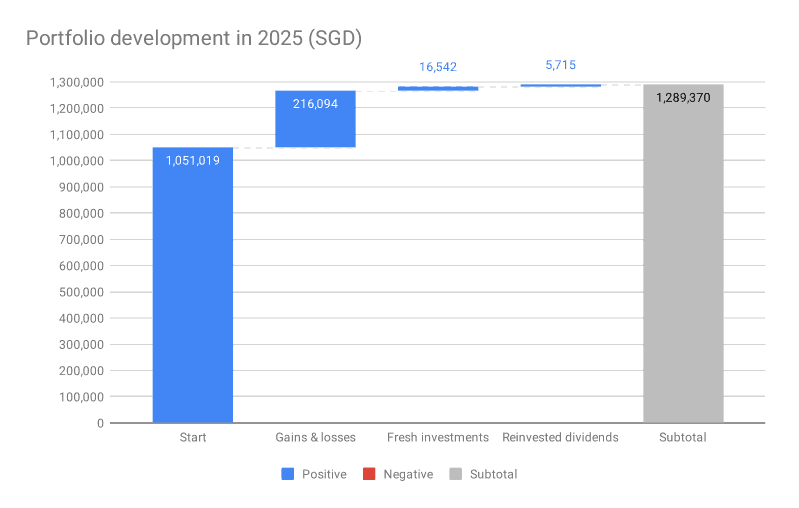

My portfolio ended the year at SGD 1,289,370.

In 2025, my portfolio increased by SGD 238,351, which is more than three times my current net salary.

This increase consisted of:

SGD 216,094 in market gains

SGD 16,542 in new investments

SGD 5,715 in dividends, which I reinvested

I currently try to minimize dividends, as they are taxed at close to 30 percent in Europe.

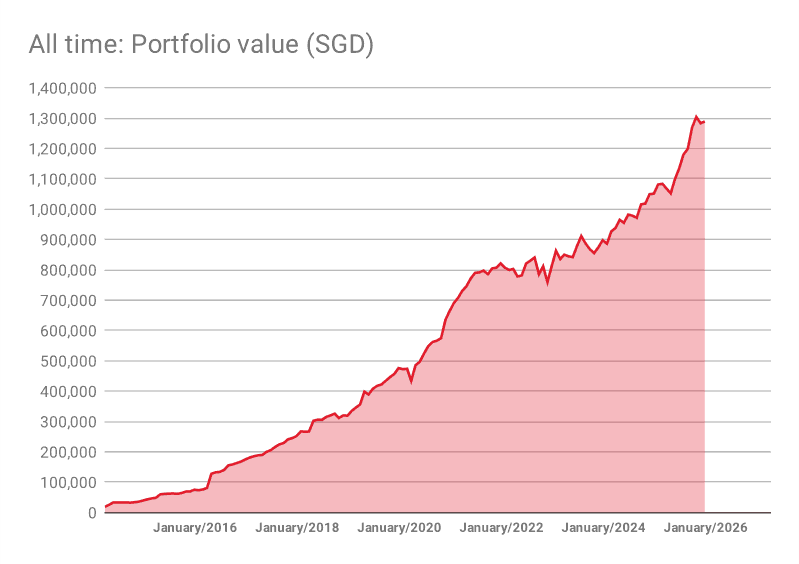

In the long run, my portfolio has been doing great:

Restructuring during the market selloff

When the United States announced its so called “Liberation Day” tariffs and markets declined sharply in April, I sold all my bonds and invested the proceeds into stock index funds. In total, I bought stock ETFs worth SGD 131,000.

This turned out to be a successful decision so far. These positions have since increased by roughly 34% and are now worth about SGD 175,000.

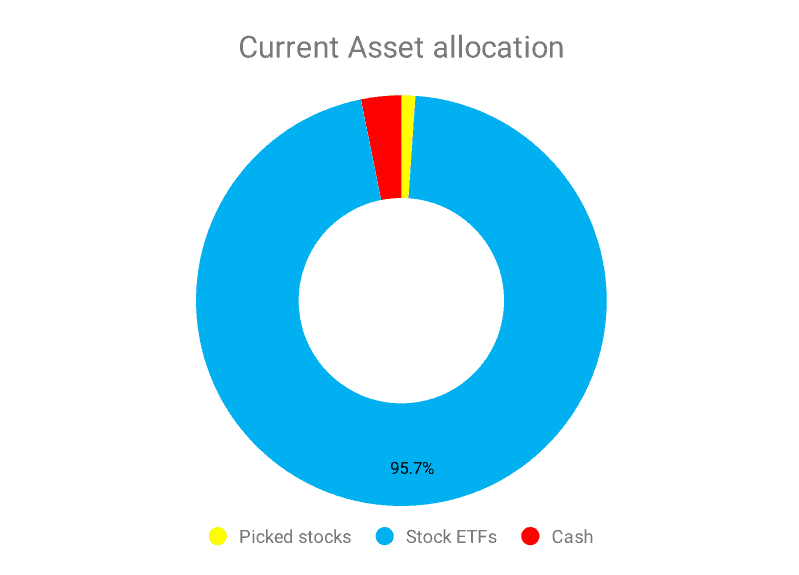

Portfolio allocation

As a result of this restructuring, my portfolio now consists of:

96 percent equities

one individual stock position, Alibaba

a small cash buffer

I currently hold no bonds.

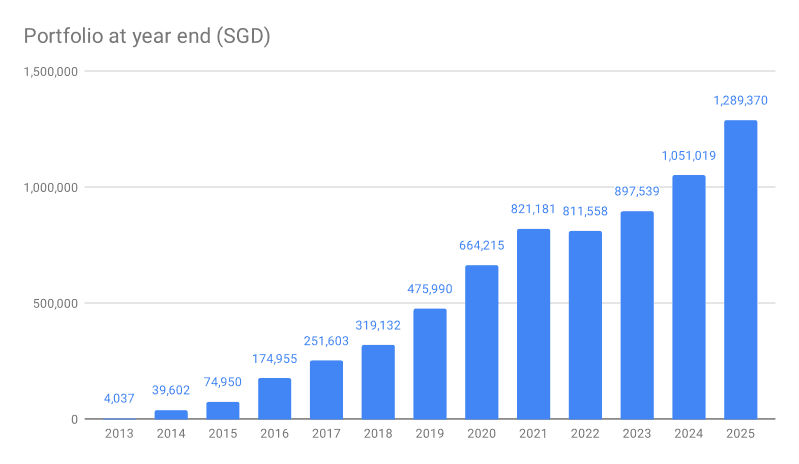

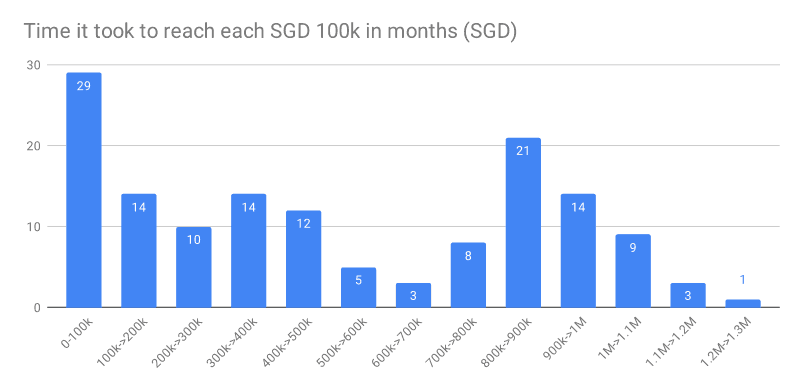

The first 100k is the hardest…

I measured how each 100k took to accumulate in the portfolio. The first 100k is clearly the hardest. Having said that, I am rather worried about the fast growth in the market lately…

Market valuation: are we in a bubble?

I am fully convinced that we are in a bubble.

Artificial intelligence is a powerful technology that will change the world, but it strongly reminds me of the railroad bubble of the nineteenth century. Enormous amounts of capital are flowing into AI long before durable, long term profits are clear. Too much capacity is being built, competition is intense, and many companies will fail to earn the returns investors expect.

The technology will succeed. Many of today’s investments will not.

Compared with the dot com boom, I suspect that many current AI companies will turn out to be the Yahoos, Altavistas, and Netscapes of the future, rather than the next Amazons or Googles.

I am also concerned that much of today’s AI discussion focuses narrowly on generative AI. While useful, it remains far from general artificial intelligence.

Under normal circumstances, I would rebalance around 30 percent of my portfolio into bonds. Doing so would trigger significant capital gains taxes in Europe, which makes it impossible / unattractive.

How I am preparing for a potential bubble burst

My options are limited, but I am doing the following:

Gradually increasing the cash portion of my portfolio

Building a larger emergency fund

Trying to reduce spending

If valuations become even more extreme, I may consider buying put options to hedge the portfolio slightly.

I am curious what others think. The inability to sell equities without severe tax consequences limits the available choices.

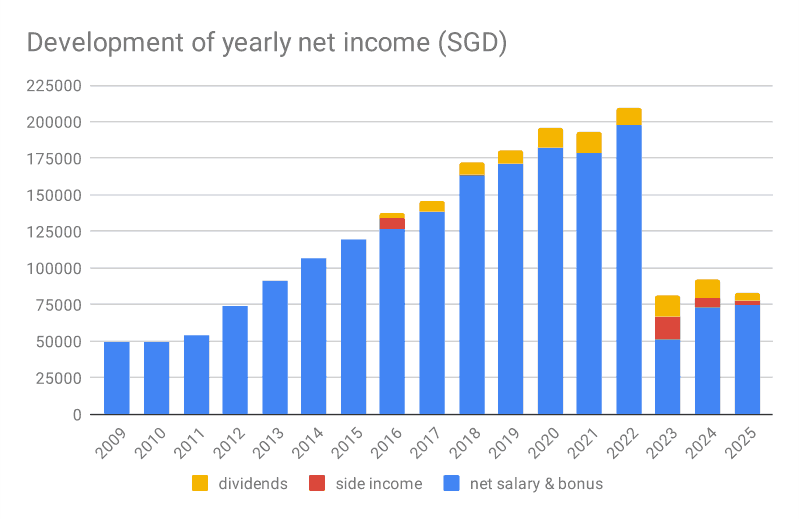

Income

Living in Europe means significantly lower salaries compared with Singapore. This is especially true in Germany, where taxes are high and gross incomes are already modest.

I hold a large equity package in the startup where I work in a leadership role. There may be upside in the future, but I do not count these unhatched chickens. Same for my two other startup investments, I count their value as zero.

My side income declined further in 2025, as I am no longer booked as frequently as a consultant in my former field. I hope to either find a new income stream or negotiate a salary increase, as my current income is too low, especially in Switzerland.

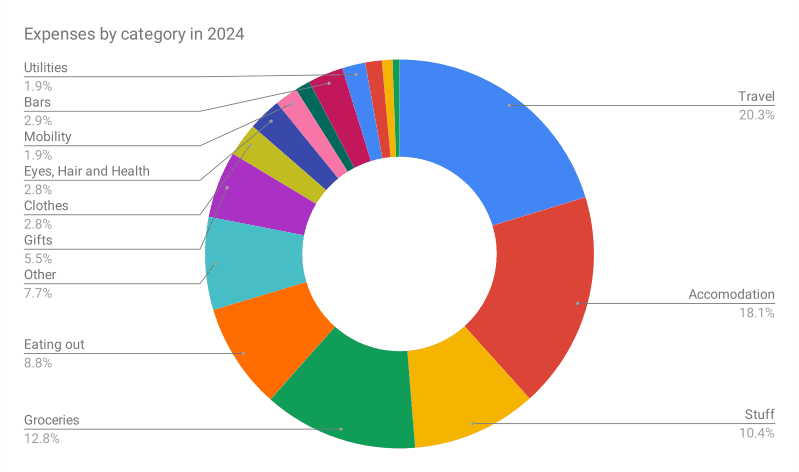

Expenses

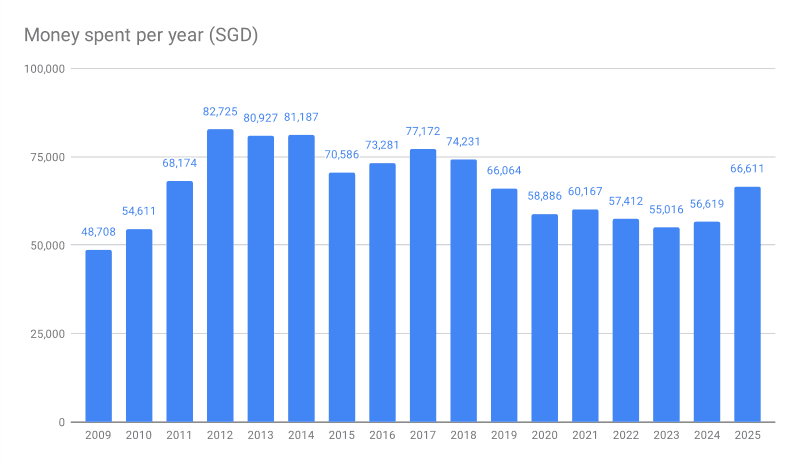

In Singapore dollar terms, my expenses increased by nearly 18% in 2025. This was mainly driven by the weakening of the Singapore dollar against the euro. In euro terms, spending increased by around 5%.

I am somewhat embarrassed by the low level of donations. On the other hand, I paid SGD 27,000 in taxes to the German government and SGD 12,000 into the dysfunctional German pension system. In total, I paid around SGD 51,000 in taxes and deductions on a relatively modest startup salary. This represents roughly 40 percent of gross income.

Taxes in Germany are super high. I miss efficient Singapore. Also the food. Have not been back to my old home since I left in 2017 – I should be called Eurovestor instead of Singvestor 🙁 I digress… Back to the topic:

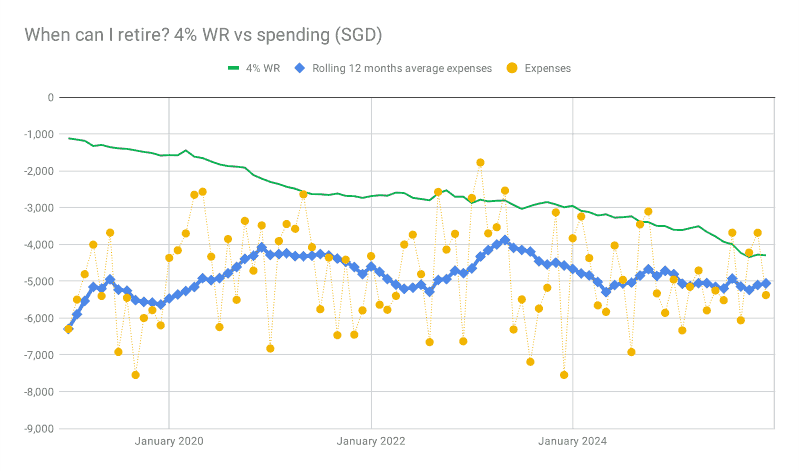

When can I retire?

This is the most important chart.

The green line shows the hypothetical income I could draw from my portfolio.

The blue line shows the trailing twelve month average of my expenses.

The yellow dots represent monthly expenses.

Once the green and blue lines intersect, I could retire even at my current spending level. Since most of my expenses are discretionary rather than essential, it would likely be possible to retire even today.

Outlook

In 2027, I will turn 45 years old, which is the age I set as my financial independence goal in the very first post on this blog twelve years ago. This makes 2026 a pivotal year.

I need to plan more concrete steps for life after retirement. I need to find new ways to structure my days and identify projects that feel meaningful.

Global stock markets have risen at a blistering pace in recent years. In my opinion, a correction or even a significant crash in 2026 is quite likely.

Good luck to everyone. I think we will need it.

Hi,

Good to see your progress for 2025 and all the best for the pivitol year 2026, although its because you shifted the goal posts earlier.

You can consider investing in Inverse S&P500 ETFs to hedge if you decide to.

Thank you! You are totally right about the shifting of the goal post. I think it is the classic “one more year” syndrome 🙂