Many of my friends are complaining this year: some got only tiny salary increases and for others their salaries even stayed flat. Gone are the days when companies in Singapore had to fiercely compete for good people and nowadays firms embark on cost cutting and optimization while cutting employee benefits. The only solution: we need to give ourselves a raise.

First we have to clarify some of the concepts:

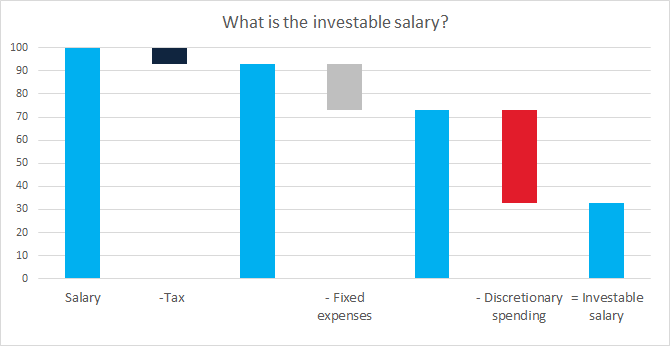

Our investable salary is the money that is leftover after tax, our fixed expenses such as rent or mobile phone plans and our discretionary spending. Discretionary spending is all the money we spend besides our fixed expenses, such as meals, vacations, shopping…

It is not just about increasing your salary

When looking to build wealth many people are obsessed with increasing their income. They work hard and as their careers and salaries improve their lifestyle changes as well. Suddenly getting a car seems like a good idea, or we need an expensive Fitness First membership to distress after the hard day at work.

This lifestyle inflation is dangerous, as very quickly you will find yourself on the hedonic treadmill.

We need to focus on improving the investable salary!

The investable salary is the only part of your income that is productive so you need to focus on increasing it. Some people spend all their salary and their investable income is zero. Some people even make the mistake to go into consumer debt, making their investable income negative.

My personal situation

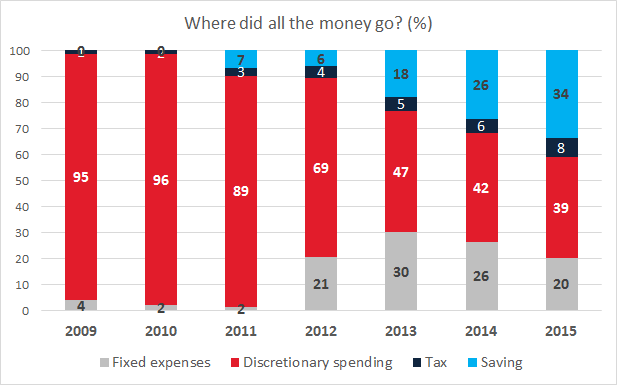

After more than seven years of full-time work I calculated where my expenses went and created the following nice graph:

The painful truth is: The first three years I used all my salary for unproductive discretionary spending to buy all the toys and useless things I felt I needed in my life. Rather stupid! In 2012 I got my act together somewhat and started saving and investing.

In 2015 I finally saved about 34% of my pre-tax salary.

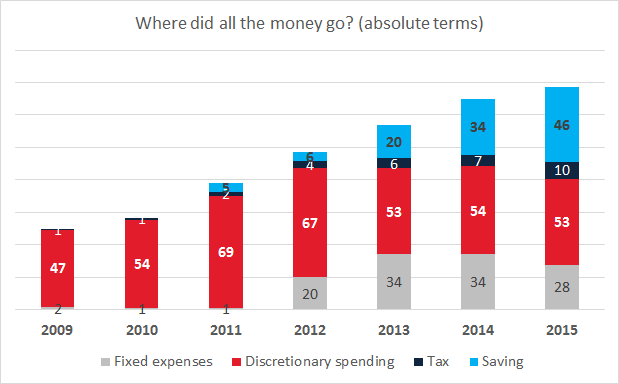

Now this looks a lot better and more responsible than it actually is. Let’s look at the figures in absolute terms:

Between 2013-2015 my discretionary spending stayed the same and I added all my salary increases to savings, avoiding lifestyle inflation.

So how to give yourself a raise?

I created this small step-by-step guide

- Step 1: Use a spreadsheet program such as Excel or a free alternative like Libre Office to calculate your salary and tax, fixed expenses and discretionary spending

- Step 2: Despair realizing how little of your salary you actually get to keep each month

Why did I spend so much money on useless stuff?

- Step 3: Optimize fixed expenses:

- 3.1: Do you still subscribe to cable TV? Cancel that and get the cheaper (SGD 14/month) Netflix if you must. Do you really need such an expensive phone plan?

- 3.2: Expensive gym memberships: Do you really use it? If no, cancel. If yes, can you find a cheaper option in a community center?

- 3.3: Do you have a car? Singapore’s most beloved status symbol, but in most cases a bottomless money pit. Do you really need it? Freeing yourself of the car will pretty much immediately free up a lot of cash-flow towards your investable income. Ignore what other people say, invest this expense instead and retire 10 years earlier.

- 3.4: Any other subscriptions or monthly expenses you can cut?

- Step 4: Reduce discretionary spending:

- 4.1: Track where your money is going each month. Meticulously note down each expense, there are free apps that can help.

- 4.2: Analyze results. Do you buy a lot of clothes? Eat out a lot? Any surprises?

- 4.3: Optimize: Set a budget in all categories and aim at a lower spending. Plan and budget all expenses.

- 4.4: Adopt some frugal habits. Explore cheaper alternatives!

- Step 5: Profit!

Making some easy adjustments to your fixed expenses and discretionary spending can often lead to a 10% increase in investable income.

Why wait for your employer to give you a raise when you can do it yourself?

Love your graph. Nothing like a visual approach to see the real situation. Sure helps to keep you motivated right? Keep suppressing/reducing the expenses while trying to increase income and we would all end up in a better place.

You are right! I just wish I had learned it a few years earlier… Nowadays I often feel like I wasted a lot of time in the first years of working

I think increasing your “investible salary” aka cut your expenses is easier when you are single and earning a high income.

For e.g. If you are a single high income earner and start off as making 150k and spending 140k, it is relatively easy to cut cost to 120k and increase your investible salary to from 10 to 30k with just a few simple changes.

However if you are a typical PMET in Singapore earning income of 70k with a family to feed and spending 60k, it is much more difficult to increase the same 10 to 30k investible salary. You will need to make deep cuts that ultimately affecting your whole family’s lifestyle. And the people around you like spouse, kids, parents, in-laws etc have to support these drastic cuts, otherwise there is the non-monetary problems that may arise.

In the latter case like me, the only option left is to wait for company to increase pay. This year I got only 2% increase which is not even enough to offset the drop in bonus due to difficult economy. In this case, I cannot even maintain the same investible income without making even more cuts.

Although cutting cost is definitely helps, my opinion is that for most people the main thing is actually climbing the corporate level and making high income. It is much easier to cut cost when you are a high income compared to middle income. Also over long term, the compounded returns from someone like Singvestor (single and high income) who is able to consistently set aside large amounts for investment will further widen the difference.

Not complaining, just regretting in my younger days do stupid things and give up good money making jobs and refuse to participate in office politics for promotion because of “work life balance”. Now want to switch also very difficult, so trap in current job saving very little every year. Hope the young ones don’t follow my footstep.

Hi Sad_PMET,

thanks for your very thoughtful post! It raises many interesting points and it really is food for thought. I tend to agree with you when it comes to the point that saving money is much easier with a higher salary. I do not want to appear like I am very good with money or a frugal person, which I am not. In many ways I have been extremely lucky. At the same time I have many friends earning much more and saving nearly nothing of their income. It is baffling, but I know people who earn 200k+ a year and still do not save any money!

I do not know your exact situation and I am no financial wizard or expert to judge. It also depends whether you have kids or parents to take care of. What I feel is that with a SGD 70k salary still a good saving rate can be achieved. CPF and mortgage payments towards an HDB flat also should of course count towards the saving rate or “investable” income. I would not focus on absolute numbers, but the saving rate is more important. You previously mentioned that you could potentially save about SGD 12/k a year. This is massive!

In the end it is about improving the gap between spending and income and the ideal approach is to work on both topics simultaneously. I personally find “MrMoneyMoustache” and “Early Retirement Extreme” very inspirational.

As we are the same age I can say this: we are still very young, aren’t we? 🙂 If we do not manage to retire early we still have a massive 28 years to work at the current retirement age. This is a lot of time to learn new skills, take more responsibility, jump ship, change jobs… Getting promoted is not too easy and in my own experience takes being very pro-active and drastically increasing responsibilities. I am not too good at that and I hate office politics, but if we challenge ourselves we might succeed. What do you think?

I had never thought of the remainder after fixed and discretionary expenses as the investable portion. I’d always called it savings, but I can see how this word shift will help my mind and habit shift. Thanks for the graphs, too. I’m a visual and verbal learner and those add a lot of understanding for me.

Thanks! Glad you like the graphs 🙂 I really enjoy making them when structuring my thoughts

Thanks for your thoughts, Singvestor! It is always good to talk with someone who is more successful than me (at least in money terms).

I LOL at the part about the 200k+ people who don’t save and can relate to them. My big boss is a good eg. His pay is >200k, but often need to ask for salary advance due to overspending. He’s like early 50s already, I wonder what’s his plan in the next 10 years.

I think what I’m doing now is like the max investible income already. Those areas you said I more or less already doing it – No car, basic cable package, no gym, xiaomi phone and dinning out with the family once a week only. Only areas can cut is the yearly family holiday and presents during occasions, if cut those the will need to sleep in the sofa.

Anything more will have to come from salary increase or promotion. I am satisfied I already do my best, just that sometimes thinking back in life last time young and stupid and made a few wrong big decisions.

Your advice to learn new things and move ahead in career is definitely agree with you. I explored changing career a year ago, but given my commitments and the need to take a significant pay cut and start from scratch decided not to in the end. Now I am just learning new things and taking up additional responsibilities slowly. I won’t reach Director or GM level, but at least can hope to move to management level.

End of the day, as long as no big unintended situation, I should be able to move up slow and steady. Early retirement seems impossible now so I will have to deal with working for another 31 years!

Truly appreciate your brutal honesty, it have made me reflect on my discretionary spending on food and superficial stuff. The theory of jotting down is definitely a strong reflection of our financial literacy and thank you for preaching that.